The Bank of Japan’s long journey is far from over Reassessing the Japanese economic cycle and its monetary policy

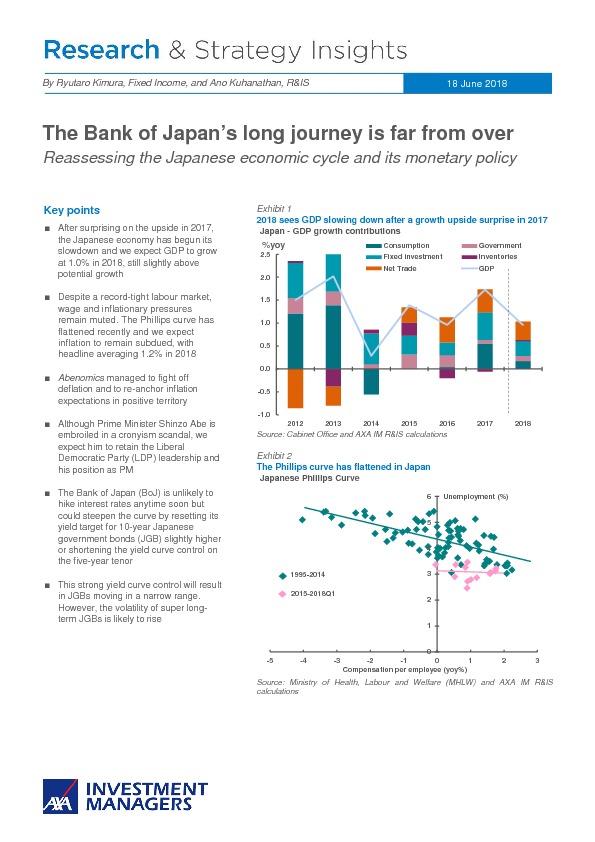

After a buoyant GDP growth in 2017, the Japanese economy began its anticipated slowdown. Gross domestic product contracted by 0.6% quarter - on - quarter (qoq) in the first three months of 2018 according to the second official estimate, worse than consensus expectations that had predicted a decline of 0.4%. Looking at the breakdown, most domestic demand categories turned negative including: inventories, consumer spending and private housing investment. While government consumption, private capital expenditure and external demand contributed positively. Domestic public demand made no contribution to the first quarter print. Although, this first quarter was impacted by unfavourable weather conditions and some other technical factors, we still expect a rebound in the second quarter and forecast GDP growth of 1% year - on - year in 2018 (Exhibit 1/consensus: +1.4%).

Our below - consensus estimate is mostly based on concerns about the labour market and its implications for household consumption. Even though there are signs of firm growth in both the number of employees in Japan and their compensation, we believe the former could be only temporary and the latter might not be strong enough to boost consumption against the backdrop of high precautionary savings.

Om dit artikel te lezen heeft u een abonnement op Investment Officer nodig. Heeft u nog geen abonnement, klik op "Abonneren" voor de verschillende abonnementsregelingen.